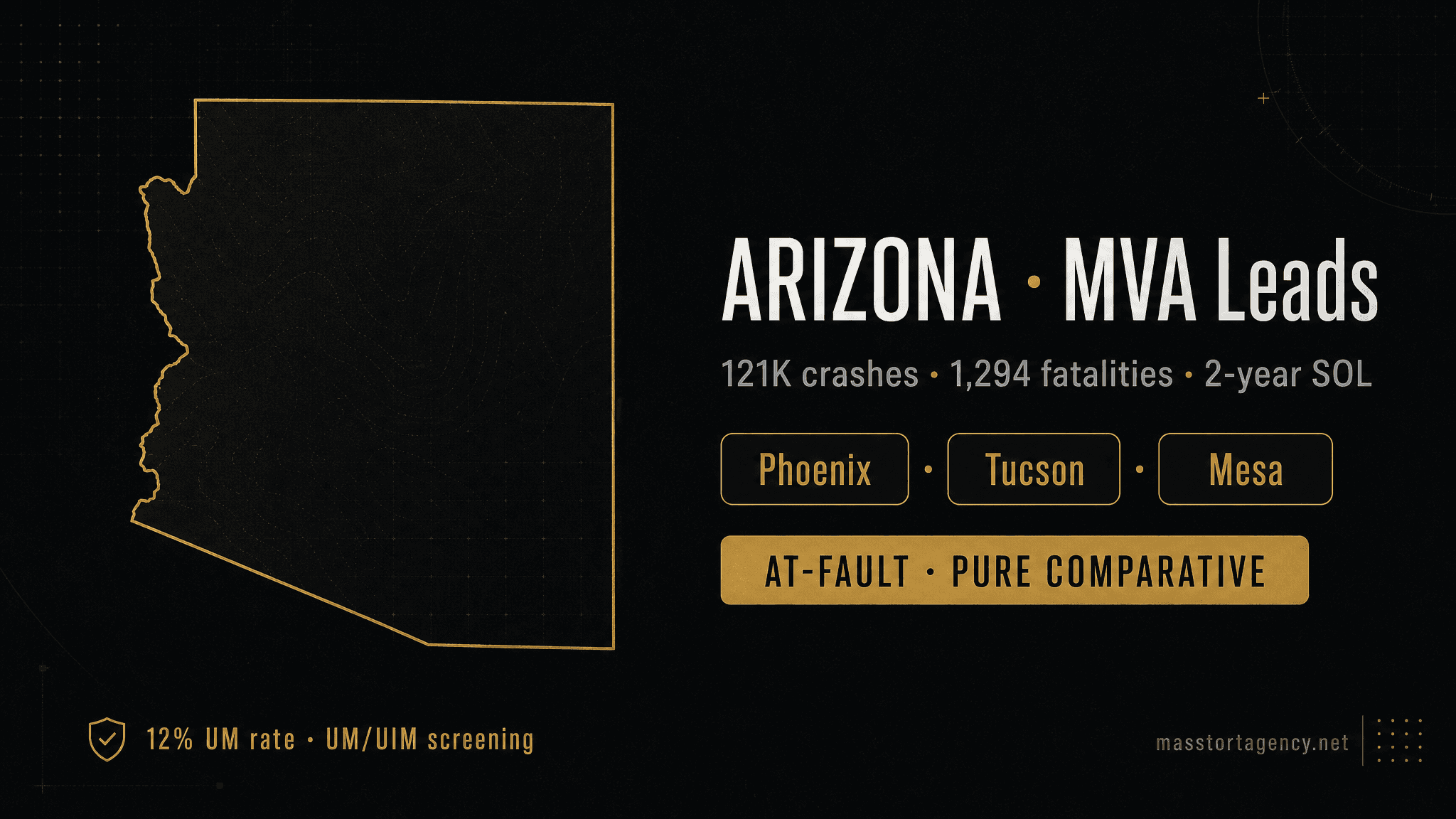

Motor Vehicle Accident Leads in Arizona

Arizona pairs pure comparative negligence (a structural case-value tailwind) with a 12% uninsured-motorist rate (a structural coverage hole). UM/UIM screening at intake is the single highest-leverage filter in the state — and Phoenix metro produces 65% of statewide volume.

Southwest

Arizona · AZ

121,000 crashes/yr

Arizona · Market Size

Source: NHTSA + AZ DOT

121,000

Reported crashes / yr

1,294

Annual fatalities

41,200

Injured claimants / yr

7.50M

State population

Arizona · Quick Reference

The 5 facts that drive Arizona MVA lead qualification

Liability

At-fault

Negligence

Pure comparative

PI SOL

2 years

PIP

Not required

Min. liability

25/50/15

Bottom line · Pure comparative + 12% uninsured rate + 25/50/15 minimums = Arizona rewards UM/UIM screening above all other intake filters. The pure-comparative advantage is real, but only collects when somebody can actually pay.

The opportunity in Arizona

Arizona MVA: pure comparative meets a 12% uninsured rate

Arizona reports 121,000 traffic crashes annually with 1,294 fatalities. Phoenix metro (Maricopa County) produces 78,400 of those crashes — 65% of statewide volume across the Loop 101 / Loop 202 / I-10 / I-17 interchange complex. Tucson adds 18,600 anchored by I-10 and the University of Arizona corridor. Mesa, Chandler, Scottsdale, and the Valley suburbs round out the practical market. The state's 7.5M residents concentrate heavily in two metros, leaving the rest of Arizona as a thin secondary market.

Arizona's structural advantage is pure comparative negligence under A.R.S. § 12-2505 — one of only 13 pure-comparative states. Claimants recover at any fault percentage, with damages reduced proportionally. A claimant 70% at fault still recovers 30% of damages. Combined with no PIP mandate, no contributory bar, and clean at-fault liability, AZ produces some of the cleanest tort math in the Southwest.

But Arizona pairs that advantage with one of the highest uninsured-motorist rates in the country. The Insurance Research Council estimates approximately 12% of Arizona drivers carry no liability insurance — and Arizona's $25K/$50K/$15K mandatory minimum is among the lower thresholds nationally. The practical effect: a meaningful share of MVA leads involve at-fault drivers without recoverable coverage. Lead vendors who don't capture the claimant's own UM/UIM and MedPay status at intake are quietly selling firms cases that look strong on liability but die on collectability.

Liability framework

How Arizona liability works — and why it matters at intake

Liability system

At-fault

Comparative negligence

Pure comparative negligence

PIP requirement

Not required

PI statute of limitations

2 years

Property damage SOL

2 years

Mandatory liability minimums

25/50/15

(BI per person / per accident / property damage, in thousands)

Arizona is at-fault: the responsible driver's carrier pays. No PIP mandate, and Arizona is one of 13 pure-comparative-negligence states — a meaningful tailwind for case value. Phoenix metro produces the bulk of statewide MVA case volume.

Arizona is a pure comparative negligence state. A claimant 80% at fault still recovers 20% of damages. Combined with the state's high uninsured-motorist rate (~12%), this raises the importance of UM/UIM screening at lead intake.

Where the volume is

Top Arizona claim markets

Phoenix metro's 78,400 crashes split across central Phoenix (downtown, Encanto, Sunnyslope), the East Valley (Mesa, Chandler, Gilbert, Tempe), the West Valley (Glendale, Peoria, Surprise, Goodyear), and the North Valley (Scottsdale, Cave Creek, Anthem). The metro is the country's fastest-growing major MSA — claimant demographics are shifting and tracker data is stale fast. Tucson carries University of Arizona and Davis-Monthan AFB overlay; Yuma sits on the I-8 / Mexico border with cross-jurisdictional complexity; Flagstaff handles I-40 / I-17 commercial vehicle and weather-pattern crashes at altitude.

Phoenix metro

78,400

Tucson

18,600

Mesa

9,800

Chandler

6,400

Scottsdale

5,900

Qualified MVA lead criteria

What "qualified" means in Arizona

In Arizona, "qualified" means clearing two gates: pure-comparative fault percentage (still recoverable at any level, but documented) and UM/UIM/MedPay coverage on the claimant's own policy (essential given the 12% uninsured rate). The seven criteria below operationalize both. Arizona vendors who skip UM/UIM capture are gambling on the at-fault driver actually having coverage — and one in eight times in AZ, they don't.

Accident date & SOL margin

Within 60 days of the wreck. Arizona's 2-year personal injury SOL compresses the case-management window — older leads burn the firm's pipeline.

Arizona jurisdiction

Accident occurred in-state with a police report on file. Report number captured at intake.

Fault apportionment

Claimant fault percentage captured. Arizona pure comparative — recovery preserved at any fault level, reduced proportionally.

Coverage profile

Arizona does not mandate PIP. Capture UM/UIM, MedPay, and health insurance status — first-dollar coverage varies widely.

Medical treatment

Active or completed care, with treatment provider documented. Injury severity captures the qualified-lead threshold.

No prior representation

Conflict-check release signed at intake. Lead is the firm's exclusive opportunity.

TCPA consent

Express written consent record on file: IP, timestamp, user agent, consent language all captured.

Arizona · Pricing benchmarks

What Arizona MVA leads actually cost in 2026

Arizona live-transfer CPL runs $265–425 — among the lowest in the Tier-1 set. Phoenix commands a 15–20% premium over statewide; Tucson and the Valley suburbs run at or below the statewide median. CPSR $1,550–2,750 reflects three structural realities: clean pure-comparative tort math when liability and coverage both exist, but a meaningful slice of cases washing out on UM/UIM coverage gaps. The numbers below reflect 2024–2026 Arizona buy cycles.

Cost per signed retainer · Arizona

$1,550–$2,750

· midpoint $2,150

Typical Arizona CPSR band, inclusive of media + intake + signed-retainer attribution. Variance driven by liability complexity and metro mix, not media cost alone.

CPL by tier

Tier 1 — Live Transfer

$265–$425

CPL · Inbound caller, pre-qualified

Tier 2 — Qualified Form

$108–$195

CPL · Form fill, screened ≤15 min

Tier 3 — Data Lead

$31–$54

CPL · Volume tier, firm-screened

How we operate in Arizona

Channel mix + compliance

Channels that work in Arizona

Phoenix and Tucson media buys are bilingual-Spanish-significant — Maricopa County and Pima County both carry meaningful Spanish-language inbound volume. Bilingual qualified-form CPL runs 8–12% above English-only; signed-retainer rate runs 4–6 points higher because vendor competition is thinner. Arizona Rule 7.3 restricts in-person, live-telephone, and real-time electronic solicitation; the Arizona State Bar enforces actively. UM/UIM claims under the claimant's own auto policy have a 6-year SOL (contract-based) versus the 2-year tort SOL — meaning UM/UIM cases have substantially longer case-management runway than third-party tort claims.

TCPA + DPPA · federal

Express written consent records on every outbound contact — timestamp, IP, user agent, consent language. DPPA enforced for any driver-record-derived data.

Arizona bar advertising rules

Arizona Rules of Professional Conduct 7.1–7.3. Direct in-person and live-telephone solicitation of MVA victims is restricted — lead vendors must source via opt-in inbound channels only.

Arizona MVA leads · FAQ

Questions Arizona firms ask before buying

Why is Arizona's pure comparative negligence advantageous for MVA case value?

Arizona is one of only 13 pure comparative negligence states. Claimants recover even at high fault percentages (e.g., 70% fault still yields 30% of damages), reduced proportionally. Compared to neighbors like Texas (51% bar) and New Mexico (pure comparative as well), AZ offers a more permissive recovery framework that supports more aggressive lead-qualification thresholds.

What is Arizona's uninsured-motorist rate and why does it matter?

Arizona has one of the highest uninsured-motorist rates in the country (~12% of drivers, per IRC data). This means a meaningful share of MVA leads will involve at-fault drivers without liability coverage — making UM/UIM screening at intake essential. Qualified AZ MVA leads should capture the claimant's own UM/UIM limits before delivery.

What's the typical CPL for buying MVA leads in Arizona?

Arizona live-transfer runs $265–425 CPL, qualified-form $108–195. Phoenix metro commands a 15–20% premium over the statewide average; Tucson and the Valley suburbs run at or below the statewide median.

Does Arizona's 2-year SOL apply to UM/UIM claims as well?

Personal injury and property damage SOL is 2 years from accident date for tort claims. UM/UIM claims are governed by contract (the claimant's own auto policy), which under Arizona law gives 6 years to file from the date of breach. The practical effect: a UM claim has a much longer runway than a third-party tort claim.

What MVA case types are most valuable in Arizona?

Commercial vehicle / trucking cases (I-10 and I-40 corridor traffic), serious-injury passenger vehicle cases, and pedestrian cases in Phoenix and Tucson. Catastrophic-injury cases in AZ benefit from the pure comparative negligence framework — case value is preserved even where shared fault is present.

Regional MVA markets